Errors in the annual accounts of the Ministry of Regional Development for 2018 exceeded CZK 5 billion. Shortcomings were also found in the management with state assets

Press Release on audit No 19/21 - 26 October 2020

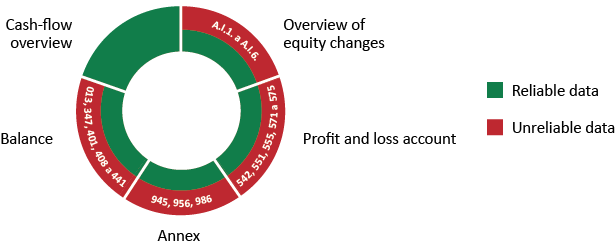

The Supreme Audit Office examined the data in the closing account, accounting management, and the preparation of the annual accounts of the Ministry of Regional Development (MoRD) for the year 2018. The auditors also focused on the data submitted by the MoRD for the assessment of the execution of the state budget. A financial statement was then drawn up from the aforementioned data. The MoRD did not have significant shortcomings in these data or in the closing account. In the annual accounts, however, the SAO found misstatements totalling over CZK 5.4 billion. The MoRD also failed to fulfil its responsibilities in the management with state assets.

Misstatements in the annual accounts were mainly caused by systemic weaknesses. Thus, in some cases, the published information on the management of the MoRD did not correspond to reality. For example, the MoRD did not correctly report on the structure of transfer costs. In the accounts, it incorrectly distinguished the share paid purely from the state budget from that which constituted pre-financing from the state budget. This share should then be borne by the budget of the European Union.

The MoRD also incorrectly accounted for corrections to errors made in previous accounting periods and only accounted for the provisioning when the liability was incurred. In doing so, it distorted the veracity of some of the published accounts. Another significant error was that the MoRD increased annually by twenty times the threshold from which it charged off-balance-sheet accounts. Thus, in the annual accounts, some accounts presented information that was not comparable, comprehensible, and reliable. Moreover, the MoRD did not account for the creation of significant contingent liabilities from existing litigation.

In the overview of changes in its equity, the MoRD provided significantly distorted and incorrect information on equity movements.

While the total value of misstatements in the annual accounts amounting to CZK 5.43 billion is substantial, it is not that significant in the context of the entire annual accounts of the MoRD. According to the SAO, some information is unreliable, but the annual accounts are not unreliable in their entirety.

The auditors did not identify material misstatements in the financial statement. While the closing account of the MoRD did not contain certain mandatory information and some other data were affected by misstatements, they, taken as a whole, had no material impact on it.

The auditors also found that the MoRD had not complied with the basic obligations in the management with state assets. For example, when renting non-residential premises in the Old Town Square in Prague in 2014, it did not negotiate a rent that would at least correspond with the level of rent that was normal in the given place and time. Premises of 674 m² were rented for CZK 3,700 per m² per year. At the same time however, similar premises were rented in this locality for CZK 27,000 per m² per year. Thus, in the period between the conclusion of the contract and the end of SAO’s audit, the MoRD reduced the revenue from state assets and the revenue of the state budget by at least CZK 41 million. In addition, the lessee did not fulfil all the agreed obligations, but the MoRD did not impose any contractual penalties. In another case, the MoRD failed to enforce a claim in court amounting to more than CZK 8 million and therefore it became time-barred.

The SAO also examined how the MoRD had remedied the deficiencies found during previous audits. Of the 17 measures, the MoRD fully and correctly implemented 11 measures, 5 partially and one measure was not implemented at all.

Reliability of the annual accounts according to individual statements

Communication Department

Supreme Audit Office